Preliminary Class 8 same dealer used truck retail sales volumes continued to rise 7.4% in May, beating expectations, according to ACT Research.

Besides a weak freight environment, stagnant freight rates and high borrowing costs, seasonality dictated a roughly 6% decline, said Steve Tam, vice president at ACT. However, auction volumes rebounded from April’s post quarter-end slump, adding 38% month-over-month in May. Wholesale activity also rose, with a 1.9% month-over-month gain.

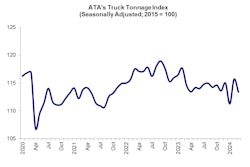

ACT Research

ACT Research

“May retail sales are typically six percentage points below normal,” said Tam. “Second quarter sales tend to be pretty average, with June as the epitome of average. Sales are also usually unremarkable in July.”

According to J.D. Power, auction volume of Class 8 sleeper tractors in May was very similar to April, which is historically typical. “On a mileage-adjusted basis, pricing for these trucks was little changed. The market was more evenly weighted between low, average and high-mileage trucks than any other month this year,” its report said.

Chris Visser, director of specialty vehicles at J.D. Power, noted that auction pricing for late-model sleepers has been surprisingly stable since March, right around the historical average on an inflation-adjusted basis.

“Incoming supply of trades and existing inventory are substantial, but some demand-side metrics are stabilizing, particularly spot freight rates,” Visser said. “Auction values seem to have found their floor in the current supply/demand environment.”

An improvement in freight demand, which looks possible in the third quarter, would support price stability and potentially a mild uptick, Visser added.

“Pricing is not currently where anyone with inventory would like it to be,” Visser concluded. “Even if there is some shoring up in summer, the market will still be more favorable for buyers than sellers."

Strength in new truck sales

Not only did April new truck builds not slow in the face of tough freight fundamentals, falling backlogs, and near-record inventories, ACT President and Senior Analyst Kenny Vieth noted production of Class 8 vehicles came in well ahead of expectations. "Still strong production and an upwards adjustment to our inventory-carrying assumptions, boosts 2024 output while reducing 2025,” he said.

“The uptick in 2024 expectations into worsening conditions is a coin toss: we may miss the timing, but shallower sooner or deeper later appear to the options,” he added. “Class 8 overcapacity persisting longer in 2024 and weighing more heavily on carrier profitability is not just a risk to Class 8, but also to the trailer forecast. If current market demand reflects EPA’27 prebuying, that prebuying comes at the expense of better freight rates sooner. While over-the-road carriers are under considerable pressure, we would be remiss not to note that vocational truck markets are in better shape than tractor markets, though even here, inventories are getting extended.”