By most indications, the freight market seems to be turning a corner, even if it is ever so slowly. That doesn’t mean business has gotten any easier for fleets – at least not yet.

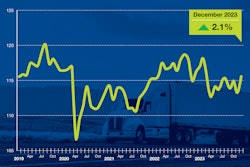

Trucking tech firm Motive has been keeping its finger on the pulse of the economy as it relates to the freight markets, and according to its January economic report, trucking saw its biggest contraction of the 2023 in December.

Joining Jason and Matt this week is Hamish Woodrow, Motive’s head of strategic analytics, who talks about the latest report and what it means for the industry.

Contents of this video

00:00 10-44 intro

00:30 Freight market

01:04 Retail index

02:53 Carrier exits

06:13 Small carriers vs. large carriers

07:52 New carrier registrations

10:18 Capacity and risk aversion

Jason Cannon:

CCJ's 10-44 is brought to you by Chevron Delo heavy duty diesel engine oil. Now there's even more reasons to choose Delo.

Matt Cole:

The trucking market continued to contract to close out 2023. What will 2024 bring?

Jason Cannon:

You're watching CCJ's 10-44, a weekly webisode that brings you the latest trucking industry news and updates from the editors of CCJ. Don't forget to subscribe and hit the bell for notifications so you'll never miss an installment of 10-44.

Hey everybody, welcome back. I'm Jason Cannon and my co-host on the other side is Matt Cole. By most indications, the freight market seems to have turned a corner, even if it's turning that corner really slowly. Now that doesn't mean business has gotten any easier for fleets, at least not yet.

Matt Cole:

Trucking tech firm Motive has been keeping its finger on the pulse of the economy as it relates to the freight markets. And according to its January economic report, trucking saw its biggest contraction of 2023 in December. Joining us this week is Hamish Woodrow, Motive's head of strategic analytics, who talks about the latest report and what it means for the industry.

Hamish Woodrow:

It's going to be an interesting time. All of 2023 has been, we had a start to the year where we saw this massive destocking, so one of the key indexes we look at is the retail index and what we saw coming through into the end of the year and peak season overall is our retail index really rebounded. So we went through an H one where we saw retailers being very, very tentative about bringing in stock. The main thing was that the inventory volumes were far too high and they were drastically trying to reduce those in the first half of last year. Finally coming in H two, we saw a more disciplined approach to restocking. We really saw the glut of inventory that built up post pandemic had really gone, and so we saw a much more normalized restocking phase. And so that was what led us to really see on our retail side is that we're finally starting to see some normalization, and we see that carrying forward into 2024.

If we really look at the last three years that we've gone through these massive structural changes, both from macroeconomic point of view with diesel prices as well as the changes to how goods move in the US and changes that COVID brought on, really impacting our view over how the supply chain looks. And it's been actually pretty unhealthy over that whole period of time. And so we're finally seeing a turn to much leaner operations and that's what we expect to happen in 2024. And a lot of those changes we're still seeing I'd say the impact of the freight bubble bursting at the end of 2022. We still see high carrier exits. December was the highest carrier exits of the year about over 4,000 carriers net exited the industry. We expect that to continue through Q1 and normalize hopefully by the end of H one. That's currently what we expect to see some tightening in the market in the backend of H one.

Jason Cannon:

As Hamish mentioned, carrier exits in December were the highest of 2023, but how much of that was just seasonal?

Hamish Woodrow:

What we saw was we saw 4,860 business, [inaudible 00:03:03] businesses, exit in December. And part of that's going to be seasonal. We always see some seasonal jumps coming through to the end of the fiscal year, driving up carrier exits. Overall, Q4 was quite large and we expect January also to have a seasonal bump as businesses just close near the end of tax years and exit, but we do still continue to see over capacity. I think what we have to realize is in 2021, the carrier market grew 27% year over year. The historical average over the 10 years is 5.7%. The biggest year before COVID was 7%. That level of expansion created this artificial bubble that is taking many quarters to go through and we continue to see that we're above where we should have been looking at the long 10-year average growth rate of this market. And so that's where we expect that we'll intersect with that in the end of Q1 to the beginning of Q2, so we're still working through over capacity. We see the spike really in December is mainly seasonal as we see a lot of businesses shut down, but fundamentally the unit economics that created this influx of carriers in 2021 with relatively low diesel prices, massive demand creating unprecedented spot prices just no longer exists. And really it's an unfavorable market, especially for the smallest carriers out there, and that's what's driven majority of our exits.

Matt Cole:

Even though carrier exits are up, are those drivers leaving the industry or just going elsewhere? Hamish will explain Motives thoughts after a word from 10-44 sponsor Chevron lubricants.

Speaker 4:

These past few years have been less than easy. We've encountered challenges we never imagined we'd ever have to deal with. From makeshift home offices and video meetings to global supply chain uncertainty, price instability, market disruptions, and everything in between. Delivering the level of services and products our customers had come to expect was difficult for all of us. We can't change what's behind us, but we can definitely learn from it. We can adapt, evolve, and take steps to reset our thinking, adapt our strategies, and restore your trust in us to better meet your needs now and in the future. That change begins today. Today we break with convention and introduce a rebalanced line of Delo heavy duty engine oils. We've reduced our product line from four categories to two. Consolidated and simplified, this lineup removes complexity from the manufacturing processes, enhancing price stability and supply chain reliability so you can trust you'll have the premium products you need to keep your business always moving forward. Our break with convention optimizes the Delo lineup to allow you to provide your customers with the best synthetic blend and synthetic heavy duty engine oils in the market, fully available at prices you can rely on. It's your assurance that you'll be well positioned to be their trusted source for proven engine protection that keeps equipment on the job giving your customers even more reasons to choose Delo.

Hamish Woodrow:

It's something that we continue to look at. And so we have a pretty diverse company set going from very large enterprise customers to a good proportion of small and medium sized businesses, and so we see a mixed picture. I think there's two things that we see is we have seen an uptick in small carriers closing down and within six months moving up into larger carriers, so the same vehicles being seen operating under different DOTs for larger carriers. So we have seen a slight uptick of a few percentages of people changing. The other thing we're seeing is type of traffic change, especially in the small carriers that they're just taking different loads or they're moving to local operations where there's still a little bit more demand. But it's something that we haven't seen, it's hard to get a full picture of and even if you look at the latest numbers from job reports, you continue to see a relatively stable overall picture in trucking.

I think some of that is we expect to be a bit lagging that we are seeing a lot of thrash in the truck sector that's not yet bubbling up to the overall economic reports put out, at least on the job report side. We expect that will probably change a little in 2024 where you get a bit better read on that, but generally we're seeing a bit of a mix. People are moving back to larger carriers, but it's a pretty tough place to be in the larger carriers. The thing we are seeing on the larger carrier side is retention is improving for those tenured employees that are at carriers. We saw a big trend in 2022 of people, or 2021 and 2022 of people leaving companies going for a better office. What we're really seeing now is retention of tenured employees has improved and that just also is an indicator of the overall job market becoming a lot tighter and there's less opportunities out there.

Jason Cannon:

New carrier registrations were also down in December, both from the previous month and the previous year. However, registrations for 2023 were still considerably higher than pre pandemic levels.

Hamish Woodrow:

If we look at Q4 overall we saw about 21,000, 20,700 carriers registered overall. That still represents 21% above our pre pandemic 2019, but it's significantly down compared to our previous years and I think December alone is 43% down versus 2021 for example, the height of this influx of new carriers. I think what we've seen is December represented the fourth consecutive month of new carrier entrants going down. What we expect is that to continue, we do expect that we're not going to go back to 2019 levels of carriers. We expect to be in the vicinity of about 10 to 15% above the 2019 average if we look at the overall 2024, but if you really look at that trend from really the peak of 2021, you've just been going to down month over month with a few peaks here or there, but we expect that to change.

The economics there, diesel price is still relatively high, spot prices are pretty low, so the kind of margins these businesses can be making in this environment isn't strong and so it does make it a tough environment for new carriers. And that included the interest rates have been overall pretty unfavorable. There's a lot of headwinds against starting a new business right now. Obviously our hope is 2024, we've already heard some interest rates cuts are on the books. I think that should help stimulate the market. That's why we're expecting a little bit increase if we look at pre pandemic.

Diesel price is pretty volatile, but it's been relatively stable over this back half of the year as long as that stays and with a bit of tightening in the backend of next year, we should see a slightly healthy environment for starting new businesses. But I think the other thing to really consider, that I think a lot is the small and medium-sized businesses are the ones that are hit most quickly by all these changes that have happened over the last few years. They're the ones that are paying retail prices on diesel. Larger carriers are generally insulated a little bit of away with contract rage or cost rates on diesel. And it's the same with spot rates, smaller carriers operating much more in the spot market and therefore are much more subjected to these massive volatilities that we've seen over the last couple of years.

Matt Cole:

Looking further into 2024, Hamish says the first half of the year will likely see similar trends as the fourth quarter with higher carrier exits before more stability going into the second half of the year.

Hamish Woodrow:

One of the things we talked about is we continue to expect contraction. We still see ourselves in a territory of over capacity. We expect contractions to continue through most of Q1 and Q2, and we expect to intersect where we should have been assuming that no pandemic had happened and created this massive influx of supply coming to end of H one. That's assuming demand stays strong, the US economy stays strong overall and nothing else happens to disrupt our 2024. And then from the retail side, we finally feel after three years of type volatility that we're really starting to get to a much more what I'll call normalized or disciplined approach from retailers. There's still a lot of risk aversion. We saw that in December we were about 2% off 2022 levels in terms of the number of visits we saw to distribution facilities for the top 50 retailers in North America.

We do expect normalization and normal restocking phase. The overall supply chain being in an over capacity will help retailers continue to manage their demand forecast and bring in stock as close to when the demand is actually going to occur, and overall we'll return to a much more lean supply chain is what we see in 2024. Those are a couple of things we're thinking from our side. We see this Q1 as a really important period of time. It's been really hard. I think for anybody operating in this sector right now, what do you do? You've all become a macro economist and every company trying to be like, okay, what do we do as a company? What do we have to do... And what we've seen is a lot of risk aversion and that's actually driving a lot of decisions right now, especially something that's really important to consider and we consider a lot is we shouldn't neglect the interest rate component.

Capital costs a lot now, and that's both in your physical assets you buy, but also in inventory decision making. It now costs you a lot more to hold inventory because that's capital on your books and debt is expensive right now, and as long as that continues to be a theme, that's something that will continue to impact all decision making. Where it's bad to be in an overstock scenario, it's bad to be... And so we're going to see probably a continual emphasis throughout 2024. Really, how do you make your business as lean as possible because it's been almost a decade where people haven't really considered a lot of these impacts that practitioners in the past have thought about. And so that's something that we consider a lot, that is a constant thought process that has been entered into almost every supply chain manager, purchasing manager that wasn't there pre pandemic.

Jason Cannon:

That's it for this week's 10-44. You can read more on ccjdigital.com. While you're there, sign up for our newsletter and stay up to date on the latest in trucking industry news and trends. If you have any questions or feedback, please let us know in the comments below. Don't forget to subscribe and hit the bell for notifications so you can catch us again next week.