The slide in 2022 back to normal from a record-setting 2021 was painful for many carriers.

During a recent CCJ webinar sponsored by Bestpass, Jason Miller, associate professor of supply chain management at Michigan State University, and ACT Research President and Senior Analyst Kenny Vieth discussed the market forces, business conditions and supply chain issues that will impact carrier operations in 2023.

Did you miss our recent webinar: "2023 Outlook for Trucking"?

Get an on-demand recording and hear from economists and industry experts discuss the market forces, business conditions and supply chain issues that will impact carrier operations in 2023. This complimentary CCJ webinar was sponsored by Bestpass.

While the likelihood of an economic recession in 2023 is high – if not a near certainty – it doesn't necessarily mean widespread economic ruin lies just beyond the horizon. And while it may be the top economic concern, Miller said a looming recession is not necessarily inevitable.

"The strongest predictor of a true recession is how the labor market behaves," Miller said. "Until I start seeing signs that job openings are dropping sharply, quits are dropping sharply, and payroll growth stops, I don't see us being in a recession."

Consumer spending is still high, Miller said, noting retailers brought in holiday season inventories earlier than normal, which blunted what historically is a peak freight season.

[Related: Gap between contract, spot rates narrowing]

"One thing we have seen," he said, "credit card debt has increased substantially but not quite yet where it was in 2019."

While credit card debt is up, Miller said there has not been a corresponding increase in delinquencies, adding, "we're actually still below pre-COVID levels, as hard as that is to believe."

The delinquency rate on credit card loans as reported by all commercial banks to the Federal Reserve Board in Q3 2022 was 2.08%. For comparison, in Q3 2019 this rate was 2.62%. Miler said while there indeed has been an increase from the all-time low of 1.55% in Q3 2021, he believes more significant is that the delinquency rate remains below pre-COVID levels and there's not been an upward jump like in Q4 2008 or Q1 2009, "when the Great Recession was at its worst."

Vieth was more bearish on the potential of an economic recession, noting he does "believe a recession is inbound." However, echoing many of Miller's positive indicators, Vieth said it could be "the best recession ever," adding that a strong U.S. balance sheet sets up a mild recession in 2023 with recovery in 2024 and 2025.

Impact on freight

Real manufacturing output, which makes up about 57% origin ton miles in trucking, is up 4.6% year over year and is near its 2018 peak, Miller said. Wholesaling, which makes up the bulk of the balance, is up 2% year over year and up 10% from 2019.

"Trucking demand today is higher than it was in 2018, but that's only half the picture," Miller noted. "Payrolls are up substantially. In 2019, we started to see seasonally adjusted employment decline, and we're not at that point yet."

Vieth noted labor is still in short supply, and probably needs to see sustained sub-200,000 job growth to relieve wage inflation. From 2011 to 2019, job growth was about 196,000 per month. Last month it was 261,000, bringing the rolling three-month average to 289,000.

Trucking profitability is at near-record levels but has slid each of the last two quarters. Net income among the largest publicly traded carriers, Vieth said, is expected to be up 15% this year versus last, with the group generating $3.5 billion in cash. Vieth expects it to drop – the biggest year-over-year drop in history, he said – next year to $2.5 billion, a dip of 27%.

ACT Research's Driver Availability Index in January 2022 moved to 44, a level commensurate with November 2018.

"Once we get to that 44, it really suggests the (truck driver) supply/demand balance is really starting to come into its own," Vieth said, adding that recent readings suggest that "the driver supply as it relates to the amount of work to be done is in balance."

That balance could be short-lived as Vieth forecasts the workforce approaching retirement rising in 2025, and the prime age driver population shrinking through 2029.

"It's going to be even more difficult to find drivers as we move into the recovery period (2024 and 2025)," he said. "If there's a silver lining here it's that the U.S. economy doesn't work without trucking."

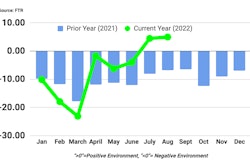

Hisotically, there's about an 18-cent-per-mile difference between contract rates and spot rates, but Vieth said it hit 66 cents in October (and 69 cents in November, according to DAT). Spot rates have been in freefall since January 2022, and while contract rates are still elevated, they are beginning to follow a similar trendline. Vieth said he expects contract rates to be down about 14% by early to mid-next year.

Spot rates could rebound late in 2023, depending on driver availability and trend upward through 2024.

Miller expressed concern over new housing starts heading into 2023, which would have an impact on freight volume, and even pegged single-family housing as his biggest concern headed into 2023. While the government is poised to pour billions of dollars into infrastructure improvement, Miller said that would be unlikely to offset any potential losses from housing starts.

"There will likely be some substitution," he said, "but the nature of those loads will differ dramatically and likely won't be in the same geographic regions."

![Reintroducing The Mack Anthem Rebuilt For Regional Haul[79]](https://img.ccjdigital.com/mindful/rr/workspaces/default/uploads/2026/07/reintroducing-the-mack-anthem-rebuilt-for-regional-haul79.FdrR1gEDrK.jpg?auto=format%2Ccompress&fit=crop&h=167&q=70&w=250)