Truck freight rates are climbing despite a notable drop in shipping volume, signaling a supply-driven market reset as carrier capacity tightens.

According to the latest U.S. Bank Freight Payment Index, released in collaboration with DAT Freight & Analytics, pricing power is shifting back to carriers ahead of any broad recovery in freight demand.

Truckload rates surge as capacity tightens

Approximately 88,000 carrier authorities have been revoked or surrendered since the dawn of the freight recession in mid-2022, according to FMCSA.

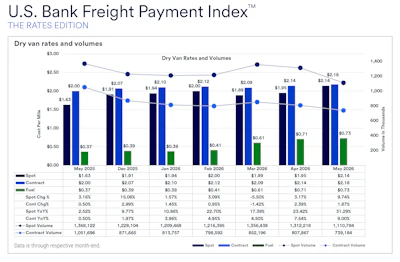

Data from the report shows a sharp year-over-year increase in dry van pricing through May 2026, led by a dramatic rebound in the spot market:

- Spot rates jumped 31.29% year-over-year, rising from $1.63 per mile in May 2025 to $2.14 per mile in May 2026.

- Contract rates climbed 9% over the same period, moving from $2.00 to $2.18 per mile.

- Fuel surcharges nearly doubled, escalating from $0.37 to $0.73 per mile.

This pricing surge occurred even as actual shipping activity dwindled. Year-over-year spot volumes fell from 1,368,122 loads to 1,110,784, while contract volumes plummeted from 1,051,696 to 739,184 loads.

The divergence indicates that capacity discipline and carrier exits—rather than strengthening consumer demand—are driving the market transformation.

Premium compression puts shippers at risk

The rapid rise in spot pricing has compressed the traditional contract premium—the gap between contracted rates and spot exposure. The spread narrowed from approximately $0.39 per mile to just $0.11 per mile.

The shrinking buffer leaves shippers increasingly exposed to market volatility. As contract rates slowly catch up to spot trends, corporate transportation budgets are facing sudden, upward pressure.

"Freight volumes may appear stable, but costs are telling a different story," said Alex Terry, director of transportation at Veritiv. "As contract rates catch up to spot pricing, shippers face growing exposure to higher transportation spend."

LTL shippers maintain pricing discipline

While the truckload sector reacts fluidly to real-time capacity shifts, the less-than-truckload (LTL) sector is relying on structural discipline to sustain margins.

Major carriers reported resilient yields for the first quarter of 2026 despite weaker volumes:

- Old Dominion reported a 7.9% year-over-year decline in daily shipments, yet managed a 4.4% increase in revenue per hundredweight (excluding fuel).

- XPO Inc. saw daily shipments rise 3.0%, while its North American LTL yield (excluding fuel) increased 4.0%.

The report concludes that freight stakeholders must prepare for an environment where the cost per mile continues to escalate, warning that operational stability does not guarantee cost stability in a supply-disciplined market.