Graphics: DAT SOLUTIONS

At the Pentagon they call it “asymmetric warfare,” but around the halls of CCJ it’s just called “trucking”: That is, a situation where combatants’ or competitors’ relative size and strength differ significantly.

For instance, the 50 largest trucking companies account for 40 percent of revenue, according to an industry overview by Dun and Bradstreet. And FMCSA estimates that there are some 500,000 active interstate motor carriers. So the big truckers are really, really big compared to everyone else.

A big carrier has some clear advantages of scale (if assets are managed properly), while smaller truckers typically profit from specialization, either in service offerings or geography.

But unless you’re one of those carriers whose revenue runs to 10 figures – in other math, those in the remaining 99.999 percent of the industry – chances are good that many, if not most, of your customers make a lot more money than you do. Several levels of magnitude more.

And, as many trucking companies know all too well, that means the relationship is a lot more important to the carrier than it is to the shipper.

That’s asymmetry, and that’s the nature of the business. It may seem ugly, or at least unfair at times. No trucking company executive or owner-op with any pride in his or her operations likes to be commoditized.

And the best way not to have your bid for a shipping contract thrown into the same hopper with some of the clowns in trucking is to emphasize superior service – and to deliver.

But you know what? That excellence still might not be enough to differentiate your company from the pack. And, in these days of precise performance measurement and cost-benefit analysis, even your great service record and you regular golf dates with shipper CEOs won’t change the math being worked up by the big computers in the back office.

All this was my long-winded windup to this: A carrier not only has to know its cost structure and a customer’s needs, a carrier must know the market in order to properly price services.

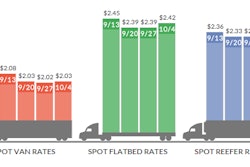

And a couple of items have come my way in the past week that offer critical insight into the market at its most dynamic – spot freight availability and pricing – and show how understanding both current and historical spot market trends should be part of every carrier’s pricing and bid strategy.

First up, DAT Solutions – which operates the DAT network of load boards – has published a white paper called “Truckload Capacity in 2014: What’s Causing the Capacity Crunch and What Can Shippers Do About it?”

Aimed at transportation and logistics managers, the paper examines truckload capacity trends from July 2013 onward (as shown in the slides above) and responds to a number of questions:

- What caused the shortage of trucks (including severe weather, HOS regulations, fleet bankruptcies, and driver shortages).

- How the shortage of capacity affected spot and contract rates.

- Which market indicators shippers and carriers can use to better understand future supply and demand conditions.

While much of the discussion of recent rate trends is an explanation for shippers, the last couple of pages focus on pricing validation and market rates.

“In recent years, as spot market pricing data has become readily available, savvy analysts are able to use this information to predict changes in shippers’ contract freight rates, often on a lane-by-lane basis,” writes Don Thornton, senior v.p. of sales and marketing at DAT Solutions.

Whether shippers are shopping for truck capacity in the spot market or not, rates are strongly influenced by the same forces that drive spot market rates, he explains. So shippers with annual bid contracts are typically slow to respond to these trends – and, I’d add for better or worse, contract carriers are locked in as well.

“The spot market, therefore, provides advance intelligence of trends in carrier capacity and pricing,” Thornton says. “This information, when included in even the simplest spreadsheet models, can help shippers, 3PLs and carriers to negotiate capacity levels for year-round availability at a sustainable price.”

And that’s the key: “sustainable price.”

Especially with capacity tight and likely to grow tighter, carriers are clearly, justifiably, anxious to take advantage of the current rate swing in their favor. Except the economic pendulum always swings back.

Having a good crystal ball – the right data – won’t prevent those swings, but it can mitigate the feast/famine free-for-all.

The DAT paper then discusses the basics of market modeling by using both internal data and external benchmarks, and pitches the company’s own DAT RateView service as just such a source of market-specific and lane-based data.

Thornton also alludes to a common complaint I hear from shippers when it comes time to review and renew a rate contract: Too many carriers, especially smaller ones, don’t have the data to support their rate requests. Shippers say they want to retain trusted carriers, but those partners must make a case that makes sense.

“This kind of transparency can lead to a dialogue between shippers and their vendors,” Thornton says, “so that instead of offering a rate increase of 5 percent or 7 percent across the board, for example, the shipper might institute market-based pricing strategies that support carriers more effectively in high-volume lanes and seasons, while adjusting some rates downward when lack of market pressure or the carrier’s costs allow for that.”

The DAT Solutions white paper can be found here.

While “big data” and modeling have been standard operating procedure at big carriers, smaller companies simply no longer can afford not to invest in the current generation of forecasting tools – especially now that the price of those tools has fallen so substantially.

It’s the cost of calculating rates on the back of an envelope that has become prohibitively expensive.

(In the second part of our look at the subtle and surprising uses of spot market data, we’ll hear from Scott Moscrip, founder and CEO of Internet Truckstop. Factoid: In addition to a Masters degree in management information systems, he also has a degree in physics. Which goes to show: You don’t have to be Bill Gates or Einstein to makes sense of the spot market, but it probably helps.)